In Conversation with Mark Mahaffey from Hindesight

Last week I caught up with an old colleague, Mark Mahaffey, who after a successful career as a trader set up the Hinde capital Gold Fund with Ben Davies. He’s now publishing an excellent investment newsletter, also on SubStack, which is focused on UK equities and dividend investing. In this 25-minute episode, we also discuss why he thinks a permanent portfolio - gold, cash, bonds, and equities in equal measure - is still his favourite portfolio idea.

Here's a bit of background about the Hindesight Newsletter:

“Written and edited by Mark Mahaffey, the HindeSight Letter has been an invaluable source of market commentary for over seven years. The newsletter is a monthly dive into not just what’s happening in the world of money and why it matters for your money, but there’s also a unique portfolio add and close alert allowing a real-time view of the why’s and crucially, when’s of closing and opening positions in FTSE 350 companies. Written with humour, style and in a way that’s simple yet powerful, it’s equally understandable for money managers and DIY investors alike.”

Adventurous Investor subscribers get a special deal on this newsletter with a 3-month, 90-day free trial. I thoroughly recommend the newsletter……

The free trial can be accessed using this link: https://hindesight.substack.com/1d62856d

Sign up and help shape your favourite funds

I mentioned this last week. Doceo is building an investor panel that will work with funds to help shape their strategy and thinking. If you like using investment trusts, this is a great chance to get your voice heard - and you could also be paid to do provide your feedback, especially if you take part in their focus groups. I think its absolutely worth doing - instead of private investors complaining about never being consulted, get paid to provide your feedback!

Sign up here to be paid for your opinions.

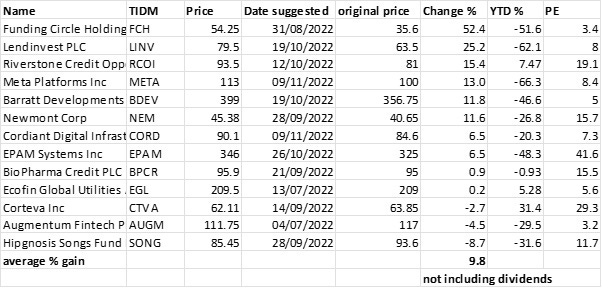

Buy list ideas Part 2

Time for the second part of my review of investment ideas for 2022, covering the period from July 1st through to December 1st.

I’ve deliberately avoided the very latest December ideas as it’s way too early for any analysis of results. Overall, I’m fairly pleased with the results, though it is very early to make any firm conclusions.

I suggested 13 ideas and the average return of the 13 ideas over the period is 9.8% in price terms. The actual total return will be much, much higher as it features a gaggle of high-income, dividend payers such as Riverstone Credit and BioPharma. I would estimate that the total return is probably well above 12.5%.

The biggest disappointment has been the loss of just under 9% on the Hipgnosis Songs Fund - I suggested this in a newsletter in September and it’s down 8.7% over the last two and a bit months. I was careful to caveat this suggestion by explaining my concerns BUT I do think the even bigger discount is now compelling. I stick with this idea and believe very strongly now that Hipgnosis will sooner rather than later either be taken over by a big corporate looking for entertainment content OR a leading private equity player looking for a cheap portfolio.

In terms of winners, I’m very pleased that my two favourite fintech plays - Funding Circle and LendInvest have both bounced off their lows to produce short-term gains of 52% and 25% respectively. I reaffirm my target of 80p for Funding Circle and 100p for LendInvest. I’m also still of the view that Riverstone Credit Opportunities will see its share price rise to closer to 100p and NAV - I have a target of 98p for the shares in the next 12 months.

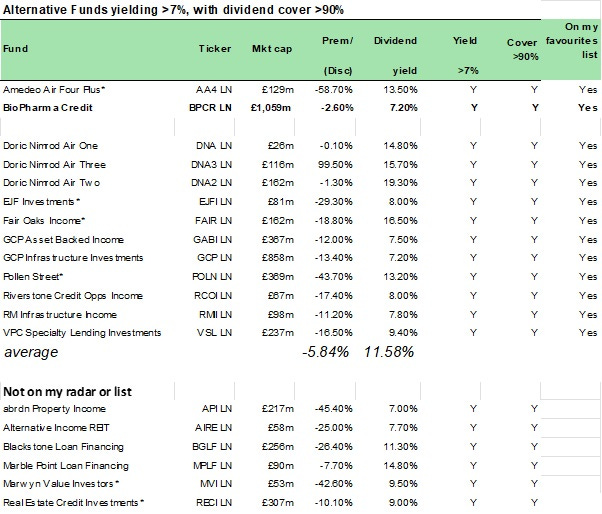

Useful Income funds list from Liberum

Last week the fund sales desk at Liberum put out a useful short note consisting of a screen of alternative listed funds that tick various boxes, namely a decent discount, a high dividend yield (over 7%) with dividend cover above 90% (I’d prefer 100%). In the resulting table below I’ve also added whether the fund highlighted is on my own preferred list - most of which are.

Looking down the list of funds that don’t feature in my watchlists, I’d make the following comments:

- Abrdn Property Income/Alternative Income REIT. I’m generally avoiding all property-based REITs at the moment as I think we are at a very dangerous moment for most property based funds

- Real Estate Credit. I do think this fund is worth a closer look but for the same reasons as above (REITs) I’d be wary about this fund as I believe we might see a sudden uptick in defaults

- Blackstone/Marble Point. I think there is certainly a place for CLO funds but my preferred vehicle is the Fair Oaks Income fund which has an excellent track record

- Marwyn is an interesting special situations private public equity vehicle with a decent track record. It trades at 42% discount to NAV despite having around 46% of the portfolio as cash. I’m not sure though this really qualifies as a regular dividend payer so wouldn’t make my list. That said on valuation grounds alone this looks interesting.

An Inflation Pivot at 4 to 6% and what that means for precious metals

A few weeks ago I was struck by the following comments from US economist Paul Krugman in the New York Times about future inflation targets. Krugman is on the side of those who think inflation will moderate and get ‘under control’, largely because the central banks are pushing us into a recession, lessening demand-side pressure. I’m probably inclined to agree with that consensus view though I understand why others think it a misguided position. Krugman’s big point though is that we need to discuss what ‘under control’ means. Will we be happy to get core rates back to 2% or maybe aim for a higher rate like 3% or even 4%?

“As it happens, a number of economists, myself included, have long argued that the 2 percent target is too low. This isn’t a radical position; many of the advocates of a 3 or even 4 percent target are as mainstream as they get. Recently, Olivier Blanchard, the former chief economist of the International Monetary Fund, made the case for 3 in The Financial Times.”

One of the most consistent stories I hear from economists now is that we should be realistic about how far we can afford to crush inflationary price pressures. I get the sense that a target of 2% is long gone and that in reality, central banks will be content - rather than ecstatic - if rates came down to a 2 to 4% band, though a 3 to 5% band might also work for them.

This represents a major shift in thinking with some potent investment implications. We are collectively a long way from the hyper inflationary scenarios mapped out by some hard money types but we are possibly in a more persistently inflationary environment than many of us imagined. As it happens a 3 to 5% range for inflation is usually fairly good news for equities as an asset class. Its also fairly good news for central banks and governments who can use these higher rates to depreciate the real value of accumulated sovereign debts. The problem with this new informal target range - publicly they’ll stick with a 2 to 3% range - is that by its nature inflation is unpredictable and its liable to blow out of that range quite quickly as geopolitics interferes.

If we are in a new normal of 4 to 6% - which I think is possible, even probable - then we are in both a more volatile world and a more inflationary world which augurs well for precious metals and especially gold and silver.

We can already see some of this thinking creeping into the spot price of gold, which as I write is a smidgeon under $1800 an ounce. In technical terms, it’s now trading above its 20-day moving average and a tiny bit below the 200 day MA.

If we think the 4 to 6% scenario is possible or even probable then I think these prices could start to push above $1800 an ounce, into a trading range between $1800 and $2000.

Solid progress for gold will be even better news for its more leveraged sibling, silver prices - traditionally silver has a high beta to gold (it outperforms in bullish markets). If that is the case then you’ll get even more leverage from silver (and gold) mining equities: top of that list would be UK-listed Mexican play Fresnillo, followed by Newmont (its mainly focused on gold but produces a lot of silver as well) which is already on my investment list plus my own favourite First Majestic Silver, a US and Canadian listed miner. This miner has a roughly 50/50 silver-gold mix of output from mines in Mexico and Nevada. The Canadian-based miner says it wants to be the world’s largest primary silver producer.

There is though one major flaw in this logic or should I say potential headwind. As I said, it seems logical to me that we are in a more volatile world where inflation targets will be hard to stick to. There is though a very real chance that inflation rates could collapse if we enter a global recession - with central banks re-opening the QE taps. In that scenario, gold will be hit hard and silver pulverized. So the downside risks are great but with China now haphazardly re-opening, I think the odds are higher that we’ll see a surprise upside inflationary blast in 2023.

Share this post